As India advances as one of the largest and fastest-growing economies in the world, the Micro, Small, and Medium Enterprise (MSME) sector is leading the way in economic expansion. With more than 63 million MSMEs operating in various sectors, it represents a significant contribution due to its role in boosting GDP, increasing exports, and creating jobs in tier-2 and tier-3 cities. However, challenges still remain for MSMEs to see their full potential. Among them is the access to adequate credit to support expansion, innovation, and scaling of operations.

The modern agricultural landscape has turned traditional practices into relics through the integration of digital technologies. The change goes beyond farming practices to encompass the underlying financial infrastructure that covers the whole value chain of agriculture.

Micro, small, and medium-sized enterprises (MSMEs) are the biggest contributors to India’s GDP. A recent 2023 study by the Minister of State for Micro Small and Medium Enterprises indicated an overall GDP contribution of 31%, while the MSME manufacturing output was up by 3.3%. This makes the sector a crucial growth engine not only for production and exports but also as an employment generator.

Agriculture remains a vital means of alleviating poverty, but a shortage of money may hinder its development. Simultaneously, agriculture is developing into a global system that demands competitive, high-quality products and is structured along value chains that frequently leave out smallholders.

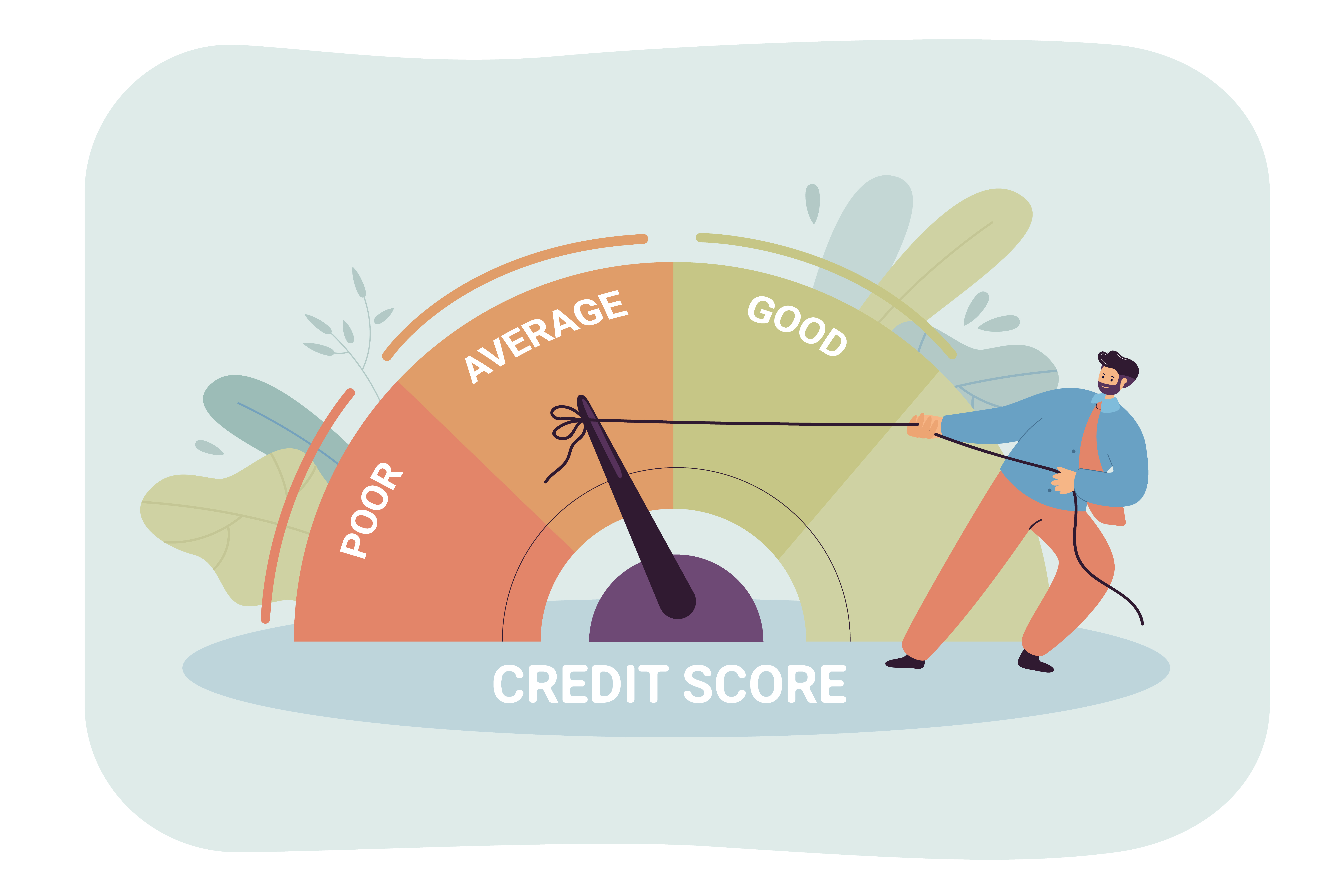

A good credit score can be a valuable financial asset. It can make obtaining loans faster or provide the borrower with lower interest rate options. For individuals who are in dire need of money, a low CIBIL score can negatively impact their ability to borrow or get a good interest rate.

The MSME sector contributes significantly to India’s economic growth. This segment’s labour-intensive nature gives job opportunities for both skilled and unskilled workers. Furthermore, this sector promotes industrial progress by providing innovative products, technologies, and advanced services. Despite all of the benefits this segment offers to our country, they continue to face many hurdles, particularly in terms of finance.

Logistics is vital in strengthening the supply chain and benefiting the economy. A laptop component manufacturing business in Tamil Nadu cannot think of connecting to the retail market in Delhi unless they have efficient transportation to carry their items and deliver them to the correct individual. Logistics plays a part in bridging the gap in the smooth flow of goods.

sme loans india / sme business loans / types of sme loans

SMEs, or Small and Medium Enterprises, are the foundation of our country’s economy. They are essential in increasing employment rates, fostering innovation, fulfilling rising population demand, and improving the economy. However, this segment’s consistent challenge is the need for readily available funds. That is where SME loans come into the picture.

unsecured business loans / best unsecured business loans

One of the prominent causes of business failure is a lack of financial help. The requirement for capital infusion in a corporation is recurring. When a company is registered, it requires finances to set up an office and hire employees, followed by funds for research and development to introduce new products, and finally, funding to market that product. Given these conditions, new-age Fintech and traditional lenders have made unsecured business loans more accessible. But what exactly are these loans, and what factors affect their interest rates? Let’s find out.

NBFC or a non-banking financial company undertakes various activities and offers both banking services and financial services. While the Indian financial system has been dominated by banks, NBFCs have been evolving rapidly since their inception in the 1960s. Today, NBFCs have become an integral part of the Indian financial system as far as lending activity is concerned. Their positive impacts have increasingly spread across different sectors. So much that the total market value of NBFCs in 2023 was around USD 326 billion.